Who is Responsible For the Banking Crisis?

In the biggest whodunit since Colonel Mustard’s fingerprints were found all over the candlestick, the blame game for whose responsible for the current global banking crisis is happening in full force.

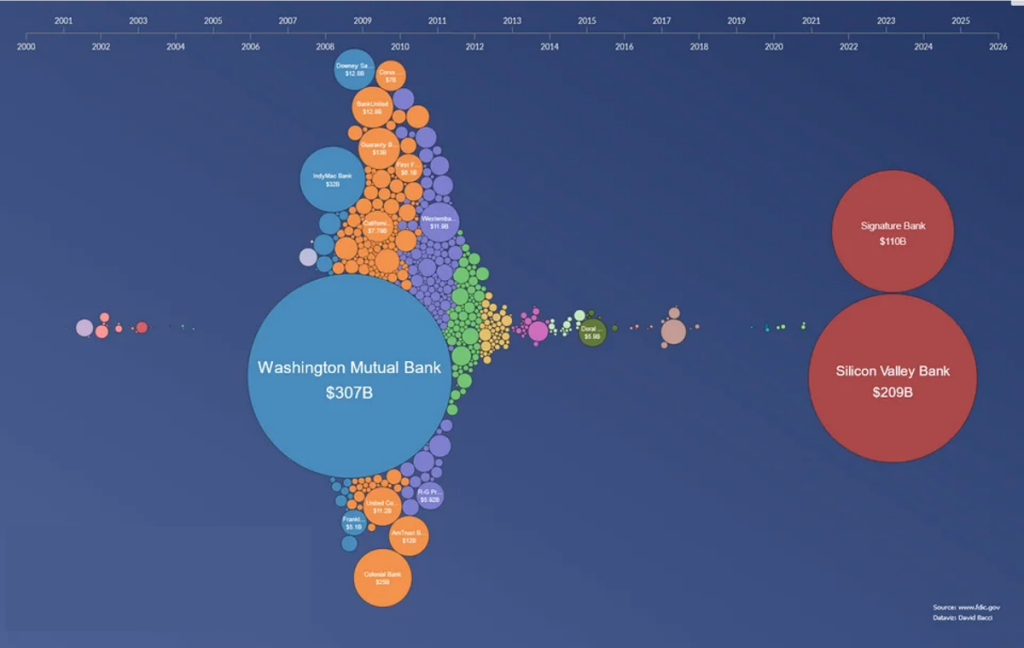

Background: The month of March has not been light on business and political drama, with some of the largest bank failures in the United States since the financial crisis. The combined failures of Silvergate Bank, Silicon Valley Bank (SVB), and Signature Bank have totaled almost a third of a trillion dollars.

US bank failures, 2001-2023

billions of USD

Right off the bat, the political accusations began:

- On the left, many were blaming the alarm bells sounded by conservative Silicon Valley venture capitalists like David Sacks, saying the panic they caused led to the run on the banks.

- On the right, “wokeism” and ESG were to blame, with US House Oversight Committee Chairman James Comer calling SVB “one of the most woke banks”.

Unfortunately: Neither of these holds much water when digging into the details. Most of the public venture capital alarm bells started after SVB was already in receivership, and the vast majority of banks with such “woke” policies as the promotion of gender equality have fared just fine.

So, what’s actually causing all these bank failures?

In short, this can really be viewed as one of the unfortunate ripples of the pandemic. Everyone knew that hitting the breaks on the entire global economy would have some impacts, and now we’re living them.

To start: In the beginning of the pandemic, with more questions than answers, governments were willing to fund lockdowns with federal stimulus and public debt. And debt was cheap after all – interest rates were cut to practically zero… so what’s the worst that could happen?

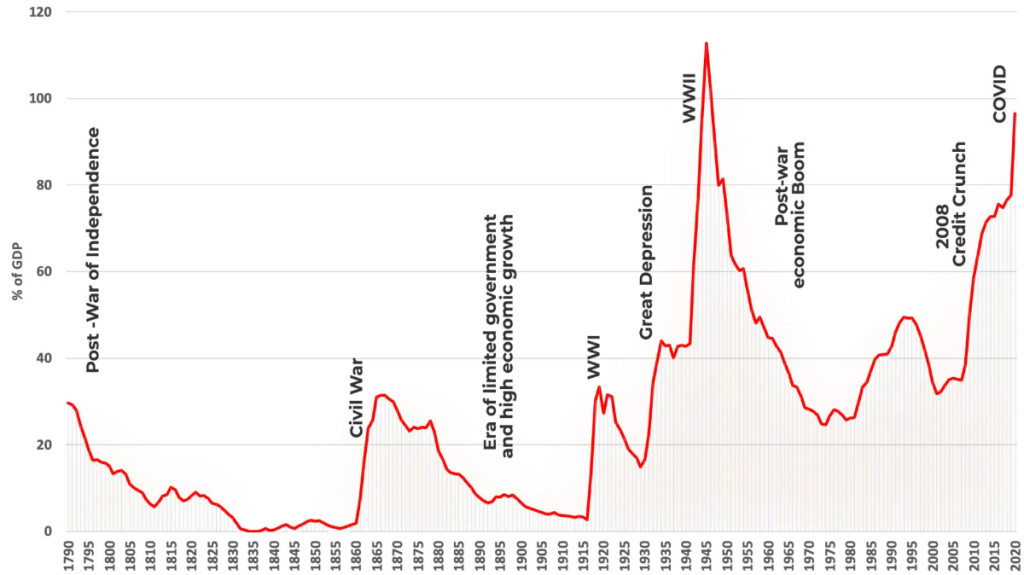

What happened: Hindsight is 20/20, but there was likely much more stimulus injected into the economy than was actually needed (remember $150,000 JPEGs of bored apes?).

US debt held by the public, 1790-2021

percentage of GDP

Starting in 2021, inflation joined the billionaire space race in trying to go to the moon, forcing central banks to raise interest rates at, in the case of the United States, its fastest rate ever.

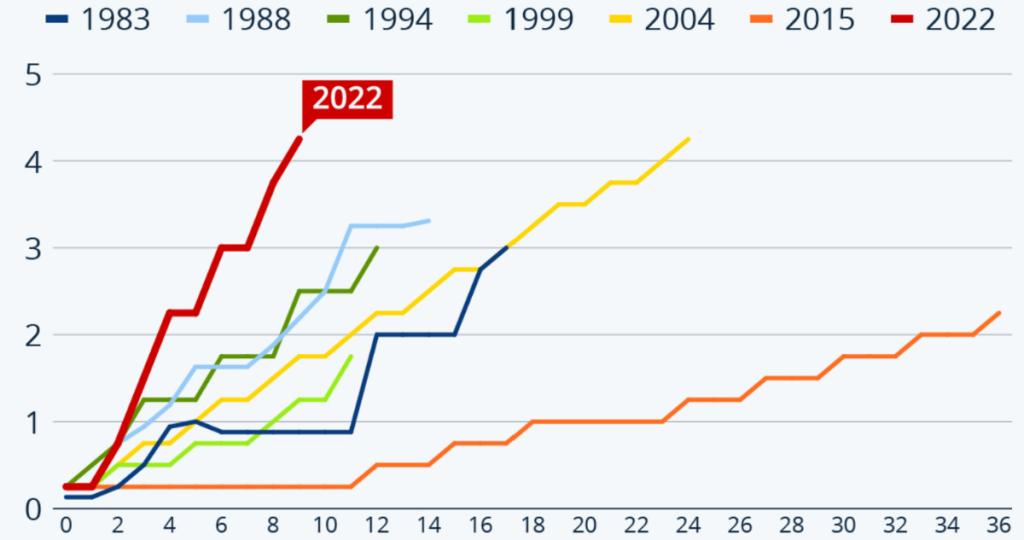

It turns out (and who could have possibly seen this coming), after US debt levels eclipsed those seen even during World War II paired with record-setting interest rate hikes and weakening of key banking regulations, debt starts to fail bringing with it the banks.

Changes in US federal funds target rate in past tightening cycles

percentage change months after first rate hike

What’s next: It’s unlikely we’ve seen the end of this banking crisis. There are more debt holders out there that will struggle with these higher interest rates. Bond traders see the Fed starting to reduce rates from here, but are now expecting higher interest rates for longer, settling out around 3 percent. Much higher than our zero-interest glory days.

Finally, what this all means for energy

First, it could mean less investment into energy transition companies. In the past, when debt was cheap, investors needed to put their money into companies just to get a return, but that’s all changed. With the option to just park money in safe, high-interest savings accounts, new companies really have to be stellar to attract investment. Marginal ideas will no longer get funded.

Governments are also going to have to reconcile with their debt problems. Over the past three years, they’ve been spending like they’re a teenager with their first credit card, but that’s coming to an end. The belt tightening exercises have begun.

- Big green subsides will increasingly have to be met within budgets, and that probably means higher taxes.

Zoom out: In the end, the murderer in this game of Clue bank failures was Mayor Green with the credit card in the lockdown room.

Of all the changes that have occurred since March 2020, the biggest might be that the days of easy spending are done, right when big spending is needed.

Copyright @ ENERGYminute Media 2024. All Rights Reserved